Updated May 2026

1. Why is the UK exporting gas when we are in short supply?

The UK has been a net importer of energy since 2004, yet gas still flows in both directions through the UK’s interconnected pipeline system. Understanding why requires a look at how the UK’s gas network actually works, and what the latest data tells us about the scale of the challenge ahead.

2. How does the UK’s gas system work?

The UK sits at the heart of a highly integrated European gas network. Gas enters the UK through domestic production from the North Sea, Norwegian pipeline imports, and LNG import terminals at Isle of Grain and South Hook. It can also flow out through interconnector pipelines to Belgium and the Netherlands.

This means gas can move through the UK to Europe when demand is lower here, and flow back when demand is higher. Since Russia’s invasion of Ukraine disrupted pipeline supplies to the continent, the UK has increasingly acted as a transit hub, with significant LNG volumes arriving and being re-exported to service European demand. These flows help balance the system across borders, but they do not reduce the need for secure domestic UK supply. If anything, they increase it.

3. Why does the UK still need its own gas?

Oil and gas currently supply around 75% of the UK’s total energy needs. Gas alone heats around 24 million homes and provides backup power to the electricity grid when wind and solar output falls short. Even as renewables grow, gas demand does not simply disappear overnight. You can find more detail on the UK’s energy mix on our Key Facts page.

Peak-day gas demand is as high as ever. Despite renewables expansion and falling average daily gas use, analysis by National Gas shows that the highest intraday peak last year required 27GW of gas supply capacity, 9% higher than the 2021 peak. The grid needs more flexible backup as intermittent generation grows, not less. On the coldest days, or when the wind does not blow, domestic gas supply is what keeps the lights on and homes warm.

Looking further ahead, even under the Climate Change Committee’s net zero pathway, the UK will still rely on oil and gas for around 20% of its energy needs in 2050. Between now and then, the UK will need somewhere between 13 and 15 billion barrels of oil equivalent. On current trajectories, the UK will produce fewer than 4 billion of those barrels domestically, meaning everything else must be imported.

4. What happens when we rely on imports instead?

Imported LNG carries a carbon footprint at least three times higher than domestically produced gas. It also comes with greater geopolitical risk and significant price exposure. UK gas prices are now closely linked to global LNG spot prices, which are driven by demand in Asia, shipping constraints, and events in the Middle East and elsewhere.

This was demonstrated clearly in early 2025, when a colder than usual winter combined with unplanned outages at Teesside CATS and Norwegian processing plants pushed the average gas price to 123p/therm in January, nearly twice the January 2024 average and the highest sustained level since the energy crisis. More recently, conflict in the Middle East has disrupted shipping through the Strait of Hormuz, through which almost 20% of global oil supplies travel, pushing crude oil prices above $100 per barrel intraday for the first time since the energy crisis peak.

The UK currently relies on LNG for around 14% of its total gas supply. Under the North Sea Transition Authority’s current projections, that figure is expected to rise to over 25% by 2030 and close to 50% by 2035. That represents a dramatic and avoidable increase in exposure to global market volatility. Our 2026 Business Outlook Report sets out the full picture on supply, demand and import dependency.

5. Could domestic production fill more of the gap?

Yes, but policy rather than geology is the constraint. The underlying resource base of the UK Continental Shelf has not changed. What has changed is the investment environment. The Energy Profits Levy, introduced in 2022 and maintained at a headline tax rate of 78%, has had a severe chilling effect on investment decisions. 2025 marked the lowest year for drilling activity since the UK’s offshore sector began, with zero exploration wells drilled for the first time on record.

OEUK’s modelling shows that with a stable and predictable fiscal and regulatory regime, the UK could unlock up to £25 billion of investment in gas projects alone, producing an additional 230 billion cubic metres of gas. Under those conditions, the UK could reduce its reliance on LNG imports to just 4 to 6% by 2030 to 2035, rather than facing a potential dependency of 25 to 50%. The full analysis is available in our 2026 Business Outlook Report.

The infrastructure picture matters here too. Around 75% of UK gas production is processed at just two terminal locations, St Fergus and Teesside. St Fergus alone handles between 25% and 50% of total UK gas flows. These are not simply commercial assets. They are critical national infrastructure. If domestic throughput falls too far and too fast, these terminals face premature closure, and once closed, they cannot readily be reinstated. The risks become significantly more likely the faster domestic production is allowed to decline through policy decisions rather than natural resource depletion.

6. Is gas compatible with the energy transition?

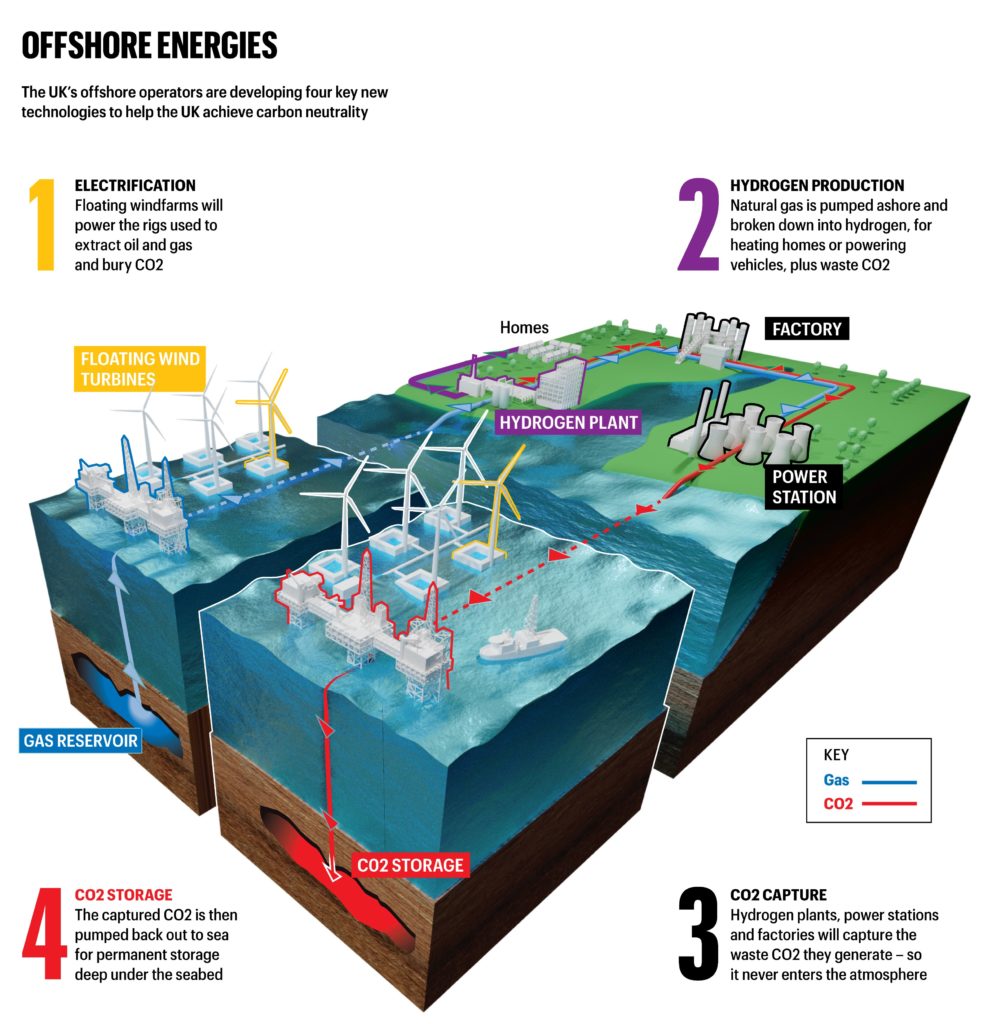

A strong domestic gas sector and the energy transition are not in conflict. They depend on each other. The same supply chains, engineering expertise and offshore infrastructure that produce gas today are the foundations for delivering offshore wind at scale, building carbon capture and storage clusters, and developing hydrogen. Between 50% and 80% of the investment required for low-carbon offshore solutions can be met by capabilities that already exist within the UK’s oil and gas supply chain.

The business sentiment picture is a warning sign. In 2025, nine out of ten supply chain companies reported they were looking overseas for growth because domestic conditions had become too difficult. The 2026 OEUK business sentiment survey shows conditions have not improved. These are the same firms that would build the UK’s offshore wind farms, carbon storage networks and hydrogen infrastructure. Losing them to overseas markets is not a cost-free outcome for the energy transition. Once capital, facilities and skilled workforces move abroad, they are very difficult to bring back. Our April 2026 Briefing Document sets out what we are asking government to do to address this.

7. Do oil and gas companies receive subsidies?

UK oil and gas production is not subsidised by taxpayers. Like other businesses, companies can offset legitimate operating costs against tax, including decommissioning, which is the complex and costly work of safely removing offshore infrastructure once production ends. This is standard business tax treatment. The sector has paid close to £450 billion in production taxes since 1970 and contributed over £36 billion to the UK economy in 2024 alone. More figures on the industry’s economic contribution are available on our Key Facts page.

8. Can oil and gas workers move into clean energy roles?

Many already do, and more can. The skills developed in oil and gas, including engineering, project management, vessel operations, safety systems and subsea work, are directly transferable to offshore wind, carbon capture, hydrogen and decommissioning. The UK oil and gas supply chain has between 60% and 80% of the capability required for future offshore carbon storage, hydrogen and floating wind. New roles in clean energy should be created alongside existing ones, not instead of them. Planning for that transition well requires continued investment in the sector now, not an accelerated decline that removes the very capabilities the transition depends upon.

9. What is the solution?

The UK needs a practical energy transition built on homegrown supply across all energy types. That means expanding offshore wind and other low-carbon technologies as quickly as possible, while producing as much of the oil and gas the UK still needs from its own waters rather than importing it from higher-carbon, less-secure sources overseas.

The UK has the resources, the infrastructure and the workforce to do this. What is needed is a stable and investable fiscal and regulatory regime that gives companies the certainty to commit capital. OEUK estimates this could unlock a £50 billion investment opportunity across the North Sea, generating significant additional tax revenues, protecting jobs, reducing emissions and strengthening the UK’s energy resilience for the long term. Our full case to government is set out in the April 2026 Briefing Document.

The gas that flows through the UK’s interconnected system, sometimes towards Europe and sometimes towards UK consumers, reflects a well-functioning regional energy market. But the underlying point is the same. Secure, affordable and lower-carbon energy for the UK starts with producing more of it at home.

Share this article