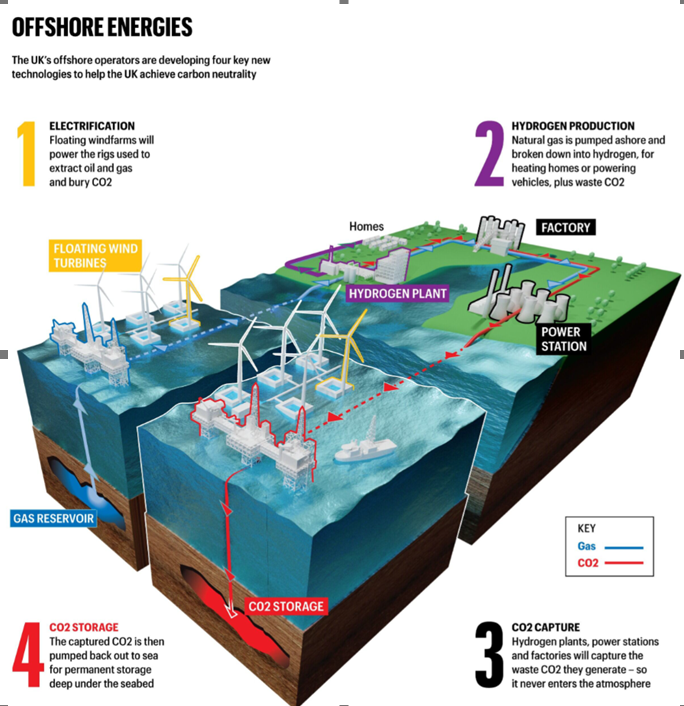

A new Carbon Capture Utilisation and Storage (CCUS) Insight published today by Offshore Energies UK shows there is a significant opportunity to repurpose existing infrastructure and capitalise on the expertise of the UK’s workforce to build a world leading CCUS industry using the UK’s strong oil and gas heritage.

The report shows that the UK has all the ingredients to become the largest carbon storage market in Europe, with 78 gigatonnes (Gt) of CO2 storage potential, which equals almost 200 years of UK emissions. Publication of this report comes ahead of the news on final investment decisions (FID) for the Track-1 clusters, Hynet and the East Coast Cluster. Together with the Track-2 clusters they will build the infrastructure needed to meet the UK’s 2030 CO2 storage target of 20-30 million tonnes per year.

The new OEUK analysis shows the scale of the opportunity and presents the case for action: the sector could create 50,000 new jobs and protect a further 100,000 in industrial regions across the UK. Carbon storage can also contribute billions to the economy between now and 2030 and be worth £100bn to the supply chain by 2050.

The report outlines six key recommendations to accelerate development of the industry:

- Simplify and enhance funding mechanisms for CCS: The government must create clearer, more predictable funding processes beyond current market pricing, which is currently insufficient for CCS. Accelerating the £20bn government support announced in 2023 and creating a route to market for transportation and storage systems and emitters outside of the “Track process” is critical to provide long-term confidence to investors.

- Leverage UK’s unique position for CCS leadership: The UK’s significant CO2 storage potential, existing infrastructure, and local supply chain give it a competitive edge in CCS. To capitalise on this policies must be developed to retain critical supply chains and prevent the need to import technologies.

- Facilitate non-pipeline and cross-border CO2 transportation: Regulatory barriers to non-pipeline CO2 transportation, especially by ship, must be removed to capitalise our storage capacity, develop an international market for CO2 storage and decarbonise non-clustered emitters.

- CCS as the key to protecting heavy industry and jobs: CCS is crucial to preserving energy-intensive heavy industries and for creating and protecting more than 150,000 jobs across the UK’s industrial heartlands. Without CCS, the UK cannot meet its net zero targets. The technology is also expected to add over £100bn to the economy by 2050.

- Strengthen carbon pricing and markets for CCS investment: A robust carbon market, including mutual recognition of UK and EU emissions trading schemes, will be critical to underpin CCS investments. Common carbon border adjustment mechanisms and a clear trajectory for carbon pricing are both essential to ensure long-term investment in CCS.

- Accelerate CCS projects for energy to meet clean power goals: Deploying carbon capture technologies in gas-fired power plants is vital to achieving the government’s 2030 clean power targets by providing low-carbon power to balance renewables . Policies must accelerate funding support for these projects to ensure they move forward.

Carbon capture will also be necessary to complement the intermittency of an electricity system increasingly based on renewables.

CO2 has been captured from natural gas processing since the 1970s. The US has thousands of kilometres of CO2 pipelines and CO2 has been stored safely under the Norwegian North Sea for over 30 years. The challenge today is to deploy these technologies at scale, at an unprecedented pace to meet our net zero targets.

Enrique Cornejo head of energy policy at Offshore Energies UK and lead author of the report said:

“There is no viable alternative to CCUS for decarbonising several energy-intensive industries, such as cement manufacturing, which contributes 7% of global CO2 emissions. To put this in perspective, if cement production were a nation, it would be the third-largest emitter in the world. Gas-fired power offset with carbon capture will also play a critical role in delivering the government’s net zero power ambitions by 2030. Low carbon power generation must come from reliable supplies that can be easily called upon when the wind doesn’t blow and the sun doesn’t shine.

“Starting work on the first two clusters is only the beginning. To fully harness the potential of CCUS and achieve the UK’s 2030 deployment targets, progress must speed up. Leaders of many projects remain uncertain about their eligibility for government support or when they can expect it. A clear plan for deployment beyond the initial clusters is critical to establish a steady flow of work for the supply chain. While 27 CO2 storage licenses have been awarded so far, more than 100 will be needed by 2050, requiring the rapid and sustained growth of the industry.

“The UK offshore sector is ready to meet the challenge, but relying on foreign expertise and technology makes little economic sense. Instead, enhancing our existing oil and gas supply chains which have highly transferable capabilities to CCUS should be a top priority.”

Share this article